Index Funds, Mutual Funds, & ETF's

Why investors need to know the differences

There is a common misconception that mutual funds, index funds and ETFs are all the same type of investment vehicles. And while there are similarities, there are also some significant differences for investors to know about. Let’s explore.

Active vs. Passive

Investors can select from two main investment strategies: active and passive portfolio management. Active portfolio management is exactly how it sounds: the portfolio manager(s) focuses on outperforming an index by “actively” making buy/sell decisions, adjusting asset allocation ranges and employing other portfolio management techniques.

Passive portfolio management on the other hand simply aims to replicate an index – not to outperform and not to underperform – but rather replicate. Therefore, there is no portfolio manager making buy/sell decisions.

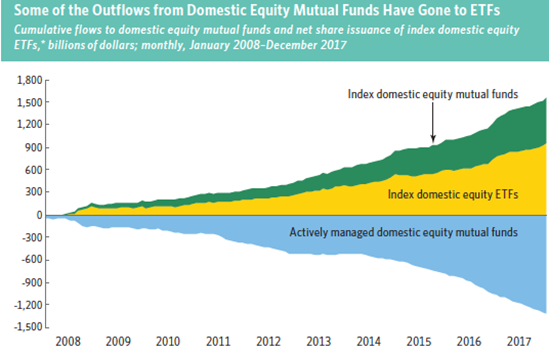

Mutual funds are either active or passive – if passive, then they are called index funds. ETFs can also be considered either passive or active.

Mutual Funds vs. Index Funds vs. ETFs

An active mutual fund is a diversified basket of securities that is professionally managed (hence the “active” term) using a combination of stocks, bonds, and cash. Mutual funds are priced at the end of every trading day – once the markets close at 4 PM EST.

Index funds are designed to track a specific index like the S&P 500 Index or Russell 2000 Index, and since they are technically mutual funds, they are also priced once a day when the markets close. But since index funds are not actively managed, generally speaking, they will offer lower costs to shareholders, relative to actively-managed mutual funds.

ETFs, like index funds, are also designed to track a specific index. But unlike mutual funds, ETFs can be traded throughout the day like a stock.

Fees Are Different and Complicated

Before we discuss the differences in fees, it’s important to remember that there are almost 10,000 different mutual funds, index funds and ETFs, so it’s impossible to speak in absolutes.

That being said, fees for index funds and ETFs are generally lower when compared to mutual funds. In fact, the Investment Company Institute reports in 2017 the following:

Mutual fund expenses – the average expense ratio of actively managed equity mutual funds fell from 0.82% to 0.78% in 2016, and the average expense ratio for actively managed bond mutual funds fell from 0.58% to 0.55%,

Index fund expenses – over that same period the average expense ratios for index equity mutual funds and index bond mutual funds remained unchanged, at 0.09% and 0.07%, respectively.

ETF expenses – in 2017, the average expense ratio of index equity ETFs fell from 0.22% to 0.21% in 2016, and the average bond ETF expense ratio went down from 0.20% in 2016 to 0.18% in 2017.

Transaction Costs

Many mutual funds charge sales commissions – as high as 5.75% for Class A shares. In addition, mutual funds might charge transaction fees of $10 or $75 per trade – both really depend on the mutual fund and how you’re buying.

Index funds don’t charge sales commissions but might have similar mutual fund transactionl fees. Again, it depends on the fund and how you’re buying.

ETFs, on the other hand, since they are traded throughout the day just like a common stock on a stock exchange, charge fees every time you make a trade (buying and selling). These fees are generally around $5-$10 per trade, so for low dollar amounts or high-frequency trading, the commissions on ETFs can really add up.

So, which are better?

Mutual funds, index funds, and ETFs have their upsides and downsides, depending on an investor’s needs. All three are fantastic tools if used properly. And they are all excellent tools allowing you diversification at a low price.

In a nutshell, a lot depends on how much you are investing right now, how often you will trade, and what amount of flexibility is needed. Additionally, it depends on the platform and the type of advisor that you're working with. For example, Weiser Financial Planning is a fee-only Registered Investment Adviser that does not sell any financial products and does not receive any commissions. Any commission or transaction fees are directly charged by the custodian. We try to reduce these costs to our clients by focusing on using No-Load, and No Transaction Fee (NTF) funds that don't carry these fees.

Sound confusing? Well, that’s why we're here to help you navigate the differences and recommend the appropriate investment vehicles for you and your family. Call me to discuss further.